Government Budget and the Economy- NCERT Notes UPSC

May 11, 2022

Navigate Quickly

Government Budget

Objectives of Government Budget

Components of Budget

Revenue Receipts

Capital Receipts

Revenue Expenditure

Capital Expenditure

Budget as a National Policy Statement

Balanced, Surplus and Deficit Budget

Measures of Government Deficit

Revenue Deficit

Implications of Revenue Deficit on the Economy

Fiscal Deficit

Implications of Fiscal Deficit

Primary Deficit

Government Debt

Perspectives on the Handling of Government Debt

Other Perspectives on Deficits and Debt

Inflationary perspective

Crowding Out perspective

Deficit Reduction

Deficit Reduction scenario in India

Suggestive Measures

Fiscal Policy of the Government

Changes is Government Expenditure

Changes in Taxes

Proportional Income Tax

Fiscal Responsibility and Budget Management Act, 2003 (FRBMA)

Main Features of the Act

Goods and Service Tax

Main Features of the Act

Differences between old tax regimes and GST

Benefits of GST

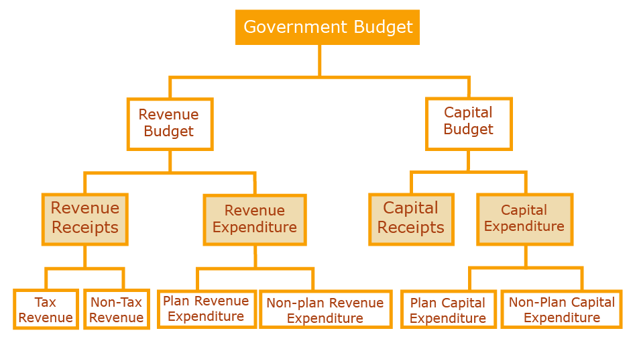

Government Budget

- It is the annual financial statement of the government.

- It shows the receipts and expenditure of the government for a particular financial year.

- Article 112 of the Indian Constitution makes a requirement in India to present before the Parliament a statement of estimated receipts and expenditures of the government in respect of every financial year which runs from 1 April to 31 March.

- The budget comprises mainly of two accounts:

- revenue account (revenue budget), that relate to the current financial year transactions; and

- capital account (capital budget), that relate to the assets and liabilities of the government.

Objectives of Government Budget

- Allocation of resources: Through budget the government allocates and mobilise resources that benefit all. This also provide public goods and services such as national defence, roads, government administration etc.

- Income redistribution:

- The government sector affects the personal disposable income of households by making transfers and collecting taxes to ensure a fair and equitable distribution of this income.

- The redistribution objective is sought to be achieved through progressive income taxation, in which higher the income, higher is the tax rate.

- With respect to indirect taxes, necessities of life are exempted or taxed at low rates, comforts and semi-luxuries are moderately taxed, and luxuries, tobacco and petroleum products are taxed heavily.

- Economic stabilisation:

- Economic stabilisation is crucial to correct fluctuations in income and employment. Any intervention by the government to expand or to reduce the aggregate demand in the economy constitutes the stabilisation function.

- The overall level of employment and prices in the economy depend upon the level of aggregate demand which in turn depends upon the spending by private and government entities.

Components of Budget

The budget primarily consists of two components such as receipts and expenditures. The receipts are further classified into revenue receipts and capital receipts whereas the expenditures are further classified into revenue expenditure and capital expenditure.

Revenue Receipts

- These receipts that do not lead to a claim on the government (that is, they neither create a liability nor decrease an asset for the government). They are divided into tax and non-tax revenues.

- Tax revenues, further are divided into:

- Direct Taxes: Like personal income tax and corporation tax etc.

- Indirect Taxes: Like excise taxes (duties levied on goods produced within the country), customs duties (taxes imposed on goods imported into and exported out of India) and service tax.

- Other direct taxes like wealth tax, gift tax and estate duty (now abolished) have never brought in large amount of revenue and thus have been referred to as ‘paper taxes’.

- Non-tax revenue, of the central government mainly consists of:

- Interest Receipts on account of loans by the central government.

- Dividends and profits on investments made by the government,

- Fees and other receipts for services rendered by the government.

- Cash grants-in-aid from foreign countries and international organisations are also included. T

- The estimates of revenue receipts take into account the effects of tax proposals made in the Finance Bill.

Important read: Economic Survey 2023 | Top 20 Key Highlights

Capital Receipts

All those receipts of the government which create liability or reduce financial assets are termed as capital receipts.

- These receipts can be debt creating or non-debt creating.

- Examples of these receipts include:

- Money received by way of Loans (Liability of future re-payment is created here).

- Money received by, sale of government assets, like sale of shares in Public Sector Undertakings (PSUs) which is referred to as PSU disinvestment, sale of assets etc. (This reduces the asset pool held by the government).

Revenue Expenditure

- It is expenditure incurred for purposes other than the creation of physical or financial assets of the central government.

- This, expenditure relates to the expenses incurred for the normal functioning of the government departments and various services, interest payments on debt incurred by the government, and grants given to state governments and other parties (even though some of the grants may be meant for creation of assets).

- Subsidies, also constitute a significant part of the Revenue Expenditure, which are incurred on under-pricing of goods, subsidised health, exports etc.

Capital Expenditure

- These are the expenditures of the government which result in creation of physical or financial assets or reduction in financial liabilities.

- This includes expenditure on the acquisition of land, building, machinery, equipment, investment in shares, and loans and advances by the central government to state and union territory governments, PSUs and other parties.

Government Budget

Budget as a National Policy Statement

- Instead of merely being a statement of receipts and expenditures, the budget has also become a significant national policy statement.

- Along with the budget, three policy statements are mandated by the Fiscal Responsibility and Budget Management Act, 2003 (FRBMA).

- The Medium-term Fiscal Policy Statement: It sets a three-year rolling target for specific fiscal indicators and examines whether revenue expenditure can be financed through revenue receipts on a sustainable basis and how productively capital receipts including market borrowings are being utilised.

- The Fiscal Policy Strategy Statement: It sets the priorities of the government in the fiscal area, examining current policies and justifying any deviation in important fiscal measures.

- The Macroeconomic Framework Statement: It assesses the prospects of the economy with respect to the GDP growth rate, fiscal balance of the central government and external balance.

Balanced, Surplus and Deficit Budget

- Balanced Budget: The government may spend an amount equal to the revenue it collects. In case the government need to incur higher expenditure, a similar amount of revenue would have to be raised, in order to keep the budget balanced.

- Surplus Budget: A situation, in which the amount of tax collection exceeds the required amount of expenditure.

- Deficit Budget: This the most common situation, in which the Government’s expenditure amount exceeds the amount of revenue raised.

Also Read : Govt Spending on Healthcare FY-2023-24 : UPSC Key Points

Measures of Government Deficit

The amount of deficit (When the spending is more than the revenue earned), can be captured in different ways, each having their own implications for the economy.

Revenue Deficit

- This refers to the excess of the Government’s revenue expenditure over its’ revenue receipts.

Revenue deficit = Revenue expenditure – Revenue receipts

- The revenue deficit includes only such transactions that affect the current income and expenditure of the government.

- Revenue deficit in 2018-19 was 2.3 per cent of GDP.

Implications of Revenue Deficit on the Economy

- It implies that the government is dissaving and is using up the savings of the other sectors of the economy to finance a part of its consumption expenditure.

- This situation means that the government will have to borrow to even finance the day-to-day consumption requirements in addition to borrowing for investments.

- High borrowing will eventually lead to high debt and interest payment obligations, which will force the government to eventually cut expenditure.

- However, since a major part of revenue expenditure is committed expenditure (in a sense that the payment obligations have already been created even before the actual payment is done for example salaries of government staff etc.), it cannot be reduced.

- Hence, often the government reduces productive capital expenditure or welfare expenditure.

- Overall, this leads to lower growth and adverse welfare implications.

Fiscal Deficit

- It is the difference between the government’s total expenditure and its total receipts excluding borrowing.

Gross fiscal deficit = Total expenditure – (Revenue receipts + Non-debt creating capital receipts)

- Non-debt creating capital receipts are those receipts which are not borrowings and, hence do not give rise to debt (E.g.: Proceeds from the sale of Public Sector Undertakings).

- These Non-debts creating capital receipts are obtained by subtracting, borrowing and other liabilities from total capital receipts.

- The fiscal deficit will have to be financed through borrowing. Thus, indicating the total borrowing requirements of the government from all sources.

- This borrowing can also be calculated as follows:

Gross fiscal deficit = Net borrowing at home (Money directly borrowed from the public through debt instruments + indirectly from commercial banks through Statutory Liquidity Ratio) + Borrowing from RBI + Borrowing from abroad

Implications of Fiscal Deficit

- It is a key variable in judging the financial health of the public sector and the stability of the economy.

- It can be seen that revenue deficit is a part of fiscal deficit (Fiscal Deficit = Revenue Deficit + Capital Expenditure - non-debt creating capital receipts).

- A large share of revenue deficit in fiscal deficit indicated that a large part of borrowing is being used to meet its consumption expenditure needs rather than investment.

Primary Deficit

The goal of measuring primary deficit is to focus on present fiscal imbalances.

- Primary deficit is calculated to obtain an estimate of borrowing on account of current expenditures exceeding revenues. It is simply the fiscal deficit minus the interest payments.

- The total borrowing requirements, of the government also include an amount incurred on account of interest payments on old, accumulated debt (loans).

Gross primary deficit = Gross fiscal deficit – Net interest liabilities

- Net interest liabilities consist of interest payments minus interest receipts by the government on net domestic lending.

Government Debt

Budgetary deficits can be financed by either taxation, borrowing or printing money. To finance such deficit the governments have mostly relied on borrowing, known as government debt.

However, if the government continues to borrow year after year, the outstanding debt accumulates causing greater interest liability, which itself can become another reason for further borrowings.

Perspectives on the Handling of Government Debt

The debt of the government can be financed by raising money through taxation or printing new currency.

- However, borrowing by the government today may create a burden on future generations, as money borrowed today may be paid by the government some decades later, financed by new taxes on the young generation, reducing their disposable incomes.

- Also, government borrowing from the people reduces the savings available to the private sector.

- There, are two broad views on the handling of government debt:

- Second view holds that households are forward-looking and will base their spending not only on their current disposable income but also on their expected future income and hence will increase their savings today.

- They will understand that borrowing today means higher taxes in the future. Further, the consumer will be concerned about future generations.

- Such an increase in household savings will offset the dissaving that the government would have to do on account of budgetary deficit and the national savings will stay at a constant level.

- This, second view is also called as the Ricardian equivalence, named after nineteenth century economists David Ricardo.

Other Perspectives on Deficits and Debt

Inflationary perspective

- One of the main criticisms of deficits is that they are inflationary.

- As increase in government spending or tax cut leads to an increase in AD.

- But firms may not be able to meet the increased demand due to which the prices of existing output will rise (Situation of Inflation).

- However, if there are unutilised resources able to match the increased AD. A high fiscal deficit is accompanied by higher demand and greater output and, therefore, need not be inflationary.

Crowding Out perspective

- When government borrows, there is a decrease in investment due to a reduction in the amount of savings available to the private sector.

- This is because if the government decides to borrow from private citizens by issuing bonds to finance its deficits, these bonds will compete with corporate bonds and other financial instruments for the available supply of funds.

- If some private savers decide to buy bonds, the funds remaining to be invested in private hands will be smaller.

- Thus, some private borrowers will get ‘crowded out’ of the financial markets as the government claims an increasing share of the economy’s total savings.

However, the above perspectives hold true under the circumstances, where the government deficit and resultant debt would not be able to augment the incomes in the economy. If due to deficit budgets, incomes see a steady rise the negative externalities can be off set.

Similarly, investment in better infrastructural facilities today may prove to be very beneficial for the future generations.

Hence, debt should not be considered burdensome at the face of it, however judged in accordance with the overall growth of the economy.

Deficit Reduction

Government deficit can be reduced by an increase in taxes or reduction in expenditure.

Deficit Reduction scenario in India

- The government has been trying to increase tax revenue with greater reliance on direct taxes as indirect taxes are regressive in nature and they impact all income groups equally.

- Receipts are being raised through the sale of shares in PSUs.

- However, the major thrust has been towards reduction in government expenditure, through better planning of programmes and better administration.

Useful links for UPSC IAS preparation:

Suggestive Measures

- Changing the scope of the government by withdrawing from some of the areas where it operated before (non-core government activities).

- As, cutting back government programmes in vital areas like agriculture, education, health, poverty alleviation, etc. would adversely affect the economy.

- However, it must be noted that larger deficits do not always signify a more expansionary fiscal policy (aiming to increase income and output through increased government spending and reduced taxes).

- The same fiscal measures can give rise to a large or small deficit, depending on the state of the economy.

- For example, if an economy experiences a recession and GDP falls, tax revenues fall because firms and households pay lower taxes when they earn less. Meaning that the deficit increases in a recession and falls in a boom, even with no change in fiscal policy.

Fiscal Policy of the Government

It is the policy by which the government adjusts its expenditure (spending) and tax rates to increase output and income and seeks to stabilise the ups and downs in the economy.

The change in Government Spending and Taxation policies impact the functioning of the economy in the following ways:

Changes is Government Expenditure

- If taxes are kept constant, and the government consumption expenditure is increased, it increases the Aggregate Demand (AD) in the economy.

- At the initial level of output, due to increased government spending, the AD would exceed the supply in the economy (as government expenditure forms a part of the AD).

- Due to the increased AD, the equilibrium would be disturbed due to which the firms would increase their production in order to meet the new levels of demand.

- This will set the market equilibrium to a point higher than before.

- This will increase the production capacity in the economy and also the incomes.

- As, under the concept of Circular Flow of Income if all income is spent on consumption then the total demand in the economy (AD) = Income (Y). Hence increased AD = Increased Y.

Changes in Taxes

- A cut in taxes increases disposable income at each level of income.

- Due to the increased disposable income, the consumption expenditure of the households will also increase, in proportion to the tax cut.

- Changes in government expenditure impact the economy directly by increasing the AD, however, changes in taxes impact this mechanism through changes in the disposable incomes of the households.

Proportional Income Tax

Under proportional income tax government collects a constant fraction, of income in the form of taxes. This kind of taxation acts as an automatic stabiliser because:

- It makes disposable income, and thus consumer spending, less sensitive to fluctuations in GDP.

- When GDP rises, disposable income also rises but by less than the rise in GDP because a part of it is siphoned off as taxes. This helps limit the upward fluctuation in consumption spending.

- During a recession when GDP falls, disposable income falls less sharply, and consumption does not drop as much as it otherwise would have fallen had the tax liability been fixed. Thus, reducing the fall in aggregate demand and stabilises the economy.

Fiscal Responsibility and Budget Management Act, 2003 (FRBMA)

The enactment of the FRBMA, in August 2003, marked a turning point in fiscal reforms, binding the government through an institutional framework to pursue a prudent fiscal policy.

Aim: That, the central government must ensure intergenerational equity and long-term macro-economic stability by achieving sufficient revenue surplus, removing fiscal obstacles to monetary policy and effective debt management by limiting deficits and borrowing.

Related Video:

Main Features of the Act

It mandates the Central Government to:

- Reduce fiscal deficit to not more than 3 percent of GDP.

- Eliminate the revenue deficit by March 31, 2009 and thereafter build up adequate revenue surplus.

- Reduction in fiscal deficit by 0.3 per cent of GDP each year and the revenue deficit by 0.5 per cent (if not achieved through the tax revenue, must be achieved by reducing expenditure).

- The actual deficits may exceed the targets specified only on grounds of national security or natural calamity or such other exceptional grounds as the central government may specify.

- The central government shall not borrow from the Reserve Bank of India except by way of advances to meet temporary excess of cash disbursements over cash receipts.

- The Reserve Bank of India must not subscribe to the primary issues of central government securities from the year 2006-07.

- Measures to be taken to ensure greater transparency in fiscal operations.

- The central government to lay before both Houses of Parliament three statements along with the Annual Financial Statement:

- Medium-term Fiscal Policy Statement

- The Fiscal Policy Strategy Statement

- The Macroeconomic Framework

- Quarterly review of the trends in receipts and expenditure in relation to the budget be placed before both Houses of Parliament.

The act applies to the central government. However, most states have already enacted fiscal responsibility legislations which have made the rule based fiscal reform programme of the government more broad based.

However, this act is for fiscal prudence there are fears that it may lead to reduction in welfare expenditure.

Since, the enactment of the FRBMA Indian economy has moved to the states of a middle income country and much has changed both domestically and globally, while affirming faith in the fiscal principles set out in the FRBM but to incorporate the changing scenario in the country for better future growth, the FRBM Review Committee had been constituted.

Goods and Service Tax

It is a single comprehensive indirect tax, operational from 1 July 2017. GST is levied on the supply of goods and services, right from the manufacturer/ service provider to the consumer.

The 101st Constitution Amendment Act was enacted to facilitate the GST. The amendment introduced Article 246A in the Constitution cross empowering Parliament and Legislatures of States to make laws with reference to Goods and Service Tax imposed by the Union and the States. Thereafter CGST Act, UTGST Act and SGST Acts were enacted for GST.

Main Features of the Act

- It is a destination-based consumption tax with facility of Input Tax Credit in the supply chain.

- It is applicable throughout the country with one rate for one type of goods or service.

- It has subsumed (replaced) a large number of Central and State taxes and cesses:

- These include Central taxes like Central Excise Duty, Service Tax, Central Sales Tax, Cesses like KKC and SBC.

- State taxes like VAT/Sales Tax, Entry Tax, Luxury Tax, Octroi, Entertainment Tax, Taxes on Advertisements, Taxes on Lottery /Betting/ Gambling, State Cesses on goods etc

- Five petroleum products have been kept out of GST for the time being but with passage of time, they will get subsumed in GST.

- State Governments will continue to levy VAT on alcoholic liquor for human consumption.

- Tobacco and tobacco products will attract both GST and Central Excise Duty.

- Under GST, there are 6 (six) standard rates applied i.e. 0%, 3%,5%, 12%,18% and 28% on supply of all goods and/or services across the country.

Differences between old tax regimes and GST

- Pre GST tax regime-imposed taxes not on the value added at each stage but on the total value of the commodity or service with minimal facility of utilisation of Input Tax Credit (ITC).

- The total value included taxes paid on intermediate goods or services amounting to cascading of tax.

- Under GST, the tax is discharged at every stage of supply and the credit of tax paid at the previous stage is available for set off at the next stage of supply of goods and/or services. It is thus effectively a tax on value addition at each stage of supply.

Benefits of GST

- Parity in taxation across the country and extend principles of ‘value- added taxation’ to all goods and services.

- It has replaced various types of taxes and cesses, levied by the Central and State/UT Governments.

- GST has simplified the multiplicity of taxes on goods and services.

- The laws, procedures and rates of taxes across the country are standardised.

- It has facilitated the freedom of movement of goods and services and created a common market in the country.

- It has also reduced the overall cost of production, which will make Indian products/services more competitive in the domestic and international markets.

- Compliance will also be easier as all tax payment related services like registration, returns, payments are available online through a common portal.

- It has expanded the tax base, introduced higher transparency in the taxation system, reduced human interface between Taxpayer and Government and is furthering ease of doing business.

Download the PrepLadder app to study from India’s top UPSC faculty and transform your UPSC CSE preparation from the Beginner level to the Advanced level. You can also join our Telegram channel for UPSC coaching and to stay updated with the latest information about the UPSC exam.

Own Your Dream

Team PrepLadder

PrepLadder IAS

Get quick access to the latest happenings across the globe. Articles revolving around factual data that aims to boost your UPSC CSE preparation and make your dreams become a reality!